It seems I just put out the last San Francisco real estate market report, and the next one already landed. Numbers are in, and you can read the entire macro and micro real estate report right here. For me, I’m an images and charts guy and sometimes get lost in words, so here are the most … Continue reading San Francisco Real Estate Market Update To End The Year 2023

Tag: Stats & Numbers

Richmond / Sunset Districts Real Estate Report

The Richmond and Sunset Districts of San Francisco continue to shine in the world of real estate. Multiple offers, and heaps of buyers out there being the norm. It’s no surprise, it’s a wonderful place to live! We went ahead and broke down the activity for both the Richmond and Sunset (includes what is also … Continue reading Richmond / Sunset Districts Real Estate Report

Buy And Sell San Francisco Real Estate Like A Pro

In this market update, we’ll help you make informed buying and selling decisions and will offer you some important guidelines for understanding home prices. We realize that buyers and sellers may feel like they’re simply guessing when it comes to determining a fair price for residential real estate, and sometimes in San Francisco that’s really … Continue reading Buy And Sell San Francisco Real Estate Like A Pro

San Francisco Real Estate Micro Market Update – Plus 3 Off Market Gems

Like a bear coming out of hibernation, the San Francisco real estate market is waking up from its Summer slumber and new inventory is flooding the market. As of the time of this post, this week alone San Francisco has seen 254 new listings (of all property types) hit the market since Monday. That’s more … Continue reading San Francisco Real Estate Micro Market Update – Plus 3 Off Market Gems

San Francisco Real Estate Market Report October 2017

Single Family Homes: September’s median sales price continued its predictable seasonal backing off from its Spring peak in May of $1,475,000, off by 8.5% to $1,350,000. Prices are still up 10.9% above September, 2016. Inventory is up from August’s 1.9 months to 2.1 months. The number of new listings on the market year-to-date is down … Continue reading San Francisco Real Estate Market Report October 2017

San Francisco Real Estate Market Report, March 2017

The San Francisco real estate market continues to experience strong buyer demand and an exceptionally low number of homes and condos for sale. The strong demand is supported by a clean sweep of positive economic indicators just posted by The Conference Board, which reported that consumer confidence is at a 15 year high, and the … Continue reading San Francisco Real Estate Market Report, March 2017

San Francisco Real Estate Market Report | February 2017

Wait for it…it’s a big Infographic loaded with data that is sure to slow down your personal gaming console, but you’ll be happy you waited. Got questions? I have answers. Just give us a shout.

State Of The Real Estate Union

If you had to guess, what would be the most common question you think a Realtor is asked? “What’s my home worth?” No. “Should I stage my home when I sell it?” No. “Do you think interest rates are going to rise?” No. All very close, and all very common questions we certainly answer more … Continue reading State Of The Real Estate Union

If It’s Not Selling Over, It’s Selling Under

Top 10 Underbids in San Francisco this past week: Address BR BA Parking List Price Sold Price Underbid 1219-1219A Stanyan Street N/A N/A 2 $2,579,000 $2,100,000 -18.57 % 1111 Bay Street 2 2.00 1 $1,199,000 $1,000,000 -16.60 % 677 Ellis Street N/A N/A 0 $2,695,000 $2,275,000 -15.58 % 338 Spear Street 2 2.00 1 $1,999,999 … Continue reading If It’s Not Selling Over, It’s Selling Under

May 2016 Central San Francisco Market Conditions

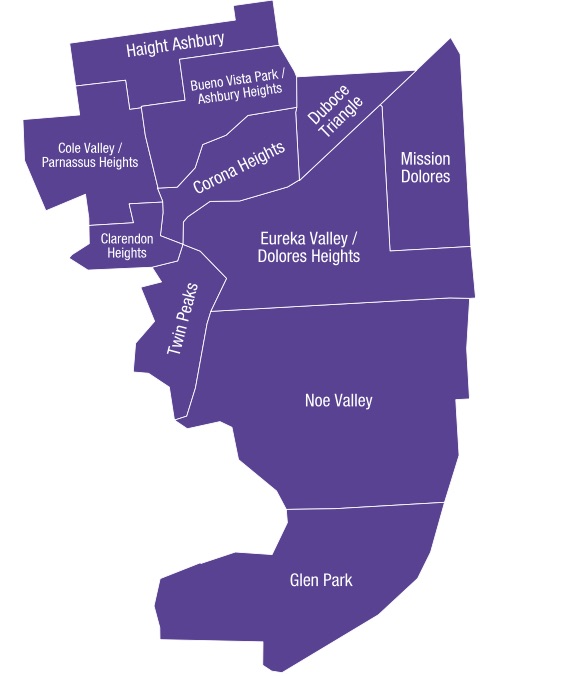

District 5’s (See SF Districts Map Here) April numbers continue their strong upwards trend with their highest ever median sales price of $2,287,500. Year-over-year, the median price is up 8.9%. Resale Condo/Loft Median Prices Resale condo-loft median prices have resumed the downward trend that started last September with a brief uptick in January and February. … Continue reading May 2016 Central San Francisco Market Conditions

May 2016 Market Report | San Francisco

We saw first quarter median Single Family Home prices in San Francisco jump with their biggest percentage increase (5.6%) in a decade, and in April’s numbers continue this strong upwards trend. The median price in San Francisco was $1,380,000 in April, the highest ever, and a 4.5% increase over March (yikes!). Resale Condo/Loft Median Prices … Continue reading May 2016 Market Report | San Francisco

San Francisco Real Estate Market Splitting In Two

The reports are starting to come in, with Paragon, Sothebys, Pacific Union, I also touched on the subject in my last sfnewsletter, and now our very own Keller Williams team reporting the same thing…a softening condo market (mostly in areas in and around SOMA), and still very robust single family homes market, especially under $1.5M, … Continue reading San Francisco Real Estate Market Splitting In Two

Golden Gate Heights Fixer Sells $455,000 Under Asking, But Still $1.9M

Hey! We’re back. What a great vacation (in Hawaii), and great to see even when I’m surfing, you’re all still browsing. So, on with the show… Monday was a travel day, so Tuesday is all about the Underbid, and this week a sweet little fixer with amazing carpeting, staging, painting, and lighting (Oh yeah, there … Continue reading Golden Gate Heights Fixer Sells $455,000 Under Asking, But Still $1.9M

San Francisco New-Home Construction Report

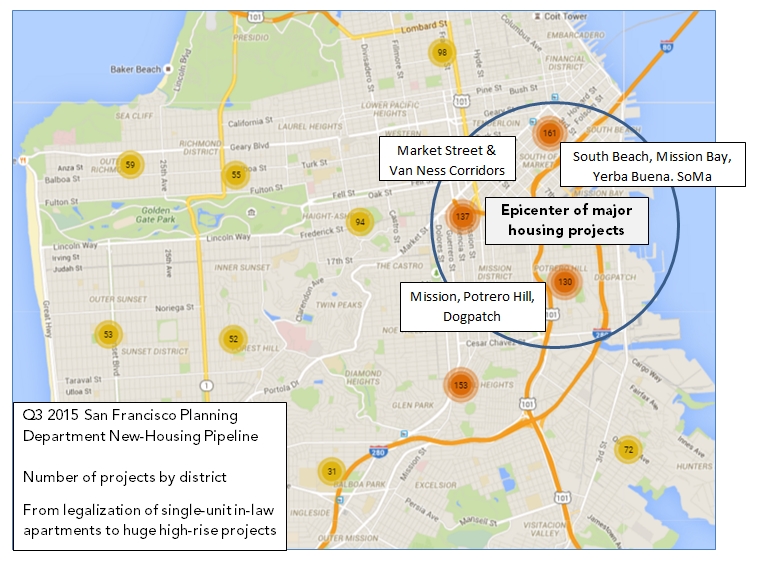

The SF Planning Department just released updated Q3 information regarding the new-housing development pipeline. San Francisco is in the midst of one of its biggest new-housing construction booms in history. (The same is occurring on the commercial development side, but this report won’t deal with that.) Indeed, it often seems that new projects of one … Continue reading San Francisco New-Home Construction Report

Housing Affordability and Market Corrections

A look at San Francisco Bay Area housing affordability trends over time and how they intersect with real estate market corrections: The 2008 San Francisco Bay Area real estate crash was not caused just by a local affordability crisis: It was triggered by macro-economic events in financial markets which affected real estate markets across the … Continue reading Housing Affordability and Market Corrections

Luxury Home Segment Cools | “Affordable” Homes Market Remains Competitive

In case you don’t get sfnewsletter (I posted this there), here is our November 2015 San Francisco Real Estate Market Report, including 11 Custom Charts: ———————————————————— San Francisco led the Bay Area and the nation when its real estate recovery began in early 2012. Within the city itself, the more affluent neighborhoods led the rebound … Continue reading Luxury Home Segment Cools | “Affordable” Homes Market Remains Competitive