Residence #7 at 4135 California Street recently closed for $4,100,000. That is an appealing $395,000 under the original asking price of $4,495,000. Penthouse units usually command top dollar, so seeing this close well under asking is definitely worth your attention. The most interesting detail of this home is the direct elevator entry taking you right … Continue reading A Great Deal in Lake Street: Penthouse Sold for $395,000 Under Asking

Category: market info

San Francisco Real Estate Update July 2026: Surging Prices, Listings Crisis

Quick Take: Single-family home prices post their strongest year-over-year gain of 2026 June brought extraordinary price appreciation to San Francisco’s single-family home market, with the median sale price climbing 26.47% year-over-year to $2,150,000. This marks the strongest annual gain we’ve seen so far in 2026. The condo market, by contrast, saw much more modest growth, … Continue reading San Francisco Real Estate Update July 2026: Surging Prices, Listings Crisis

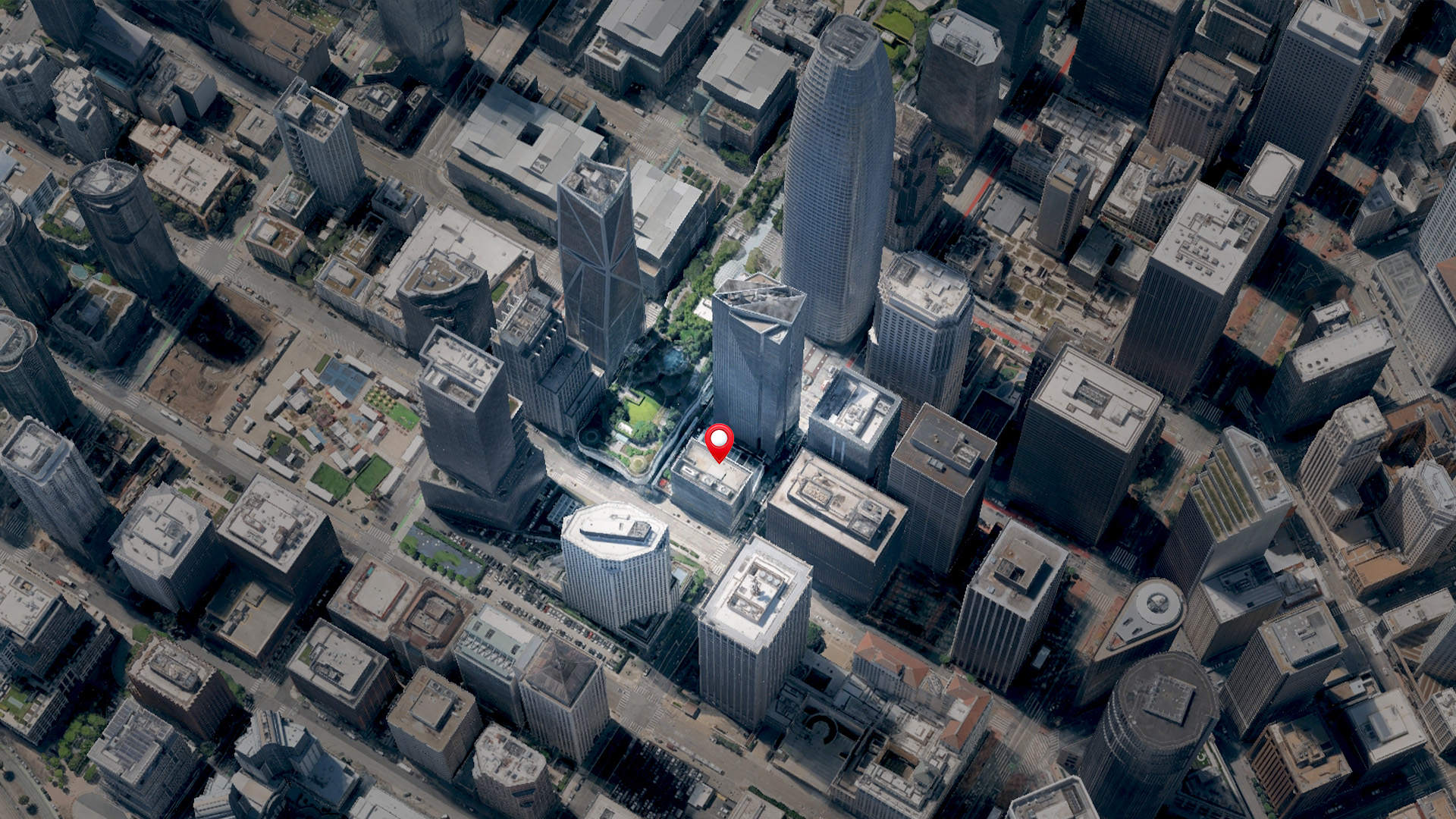

A Great Deal in South of Market: Penthouse Sold for $650,000 Under Asking

Welcome to the good life at 765 Market Street #PH2G. Perched high above downtown on one of the Four Seasons penthouse levels, this residence just closed for a staggering $650,000 under the asking price. The original list price was set at $2,750,000, and it ultimately went for $2,100,000. Sweeping South Bay and city views greet … Continue reading A Great Deal in South of Market: Penthouse Sold for $650,000 Under Asking

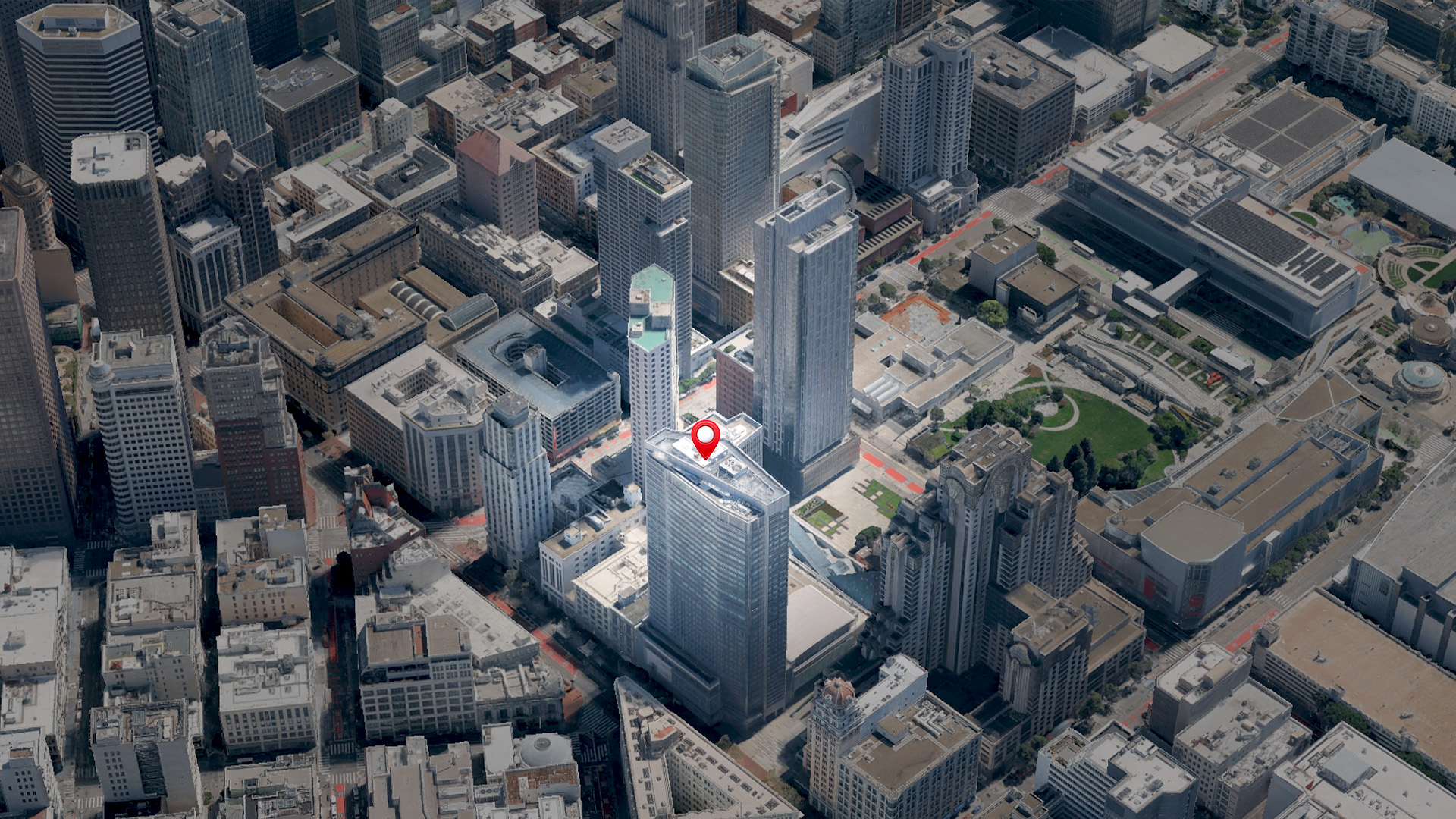

Underbid Sale in Financial District: Unit Sold for $98,000 Under Asking

We have a serious value play over at the Ritz Carlton Residences. Residence 1703 recently closed out for $1,400,000. The original asking price stood at $1,498,000. That means the buyer walked away saving $98,000 off the top… a solid win in anyone’s book. This particular property features a comprehensive interior update. Sweeping city views flood … Continue reading Underbid Sale in Financial District: Unit Sold for $98,000 Under Asking

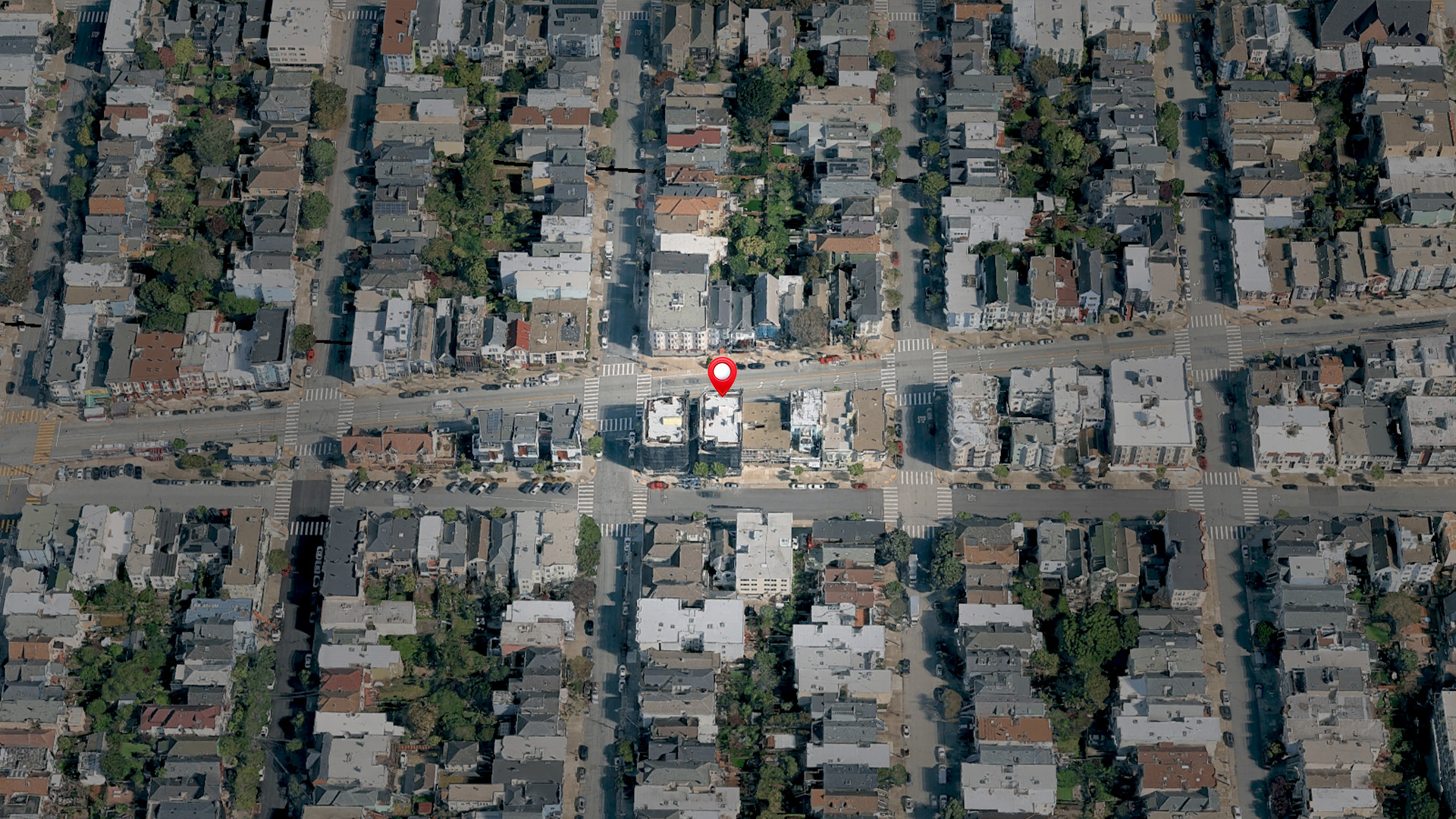

A Great Deal in Russian Hill: Unit Sold for $545,000 Under Asking

The property at 1101 Green Street Unit 1801 recently closed for $7,350,000. Buyers originally saw the listing priced at $7,895,000. Selling for an incredible $545,000 under the asking price makes this transaction highly notable… considering the city apartment includes the only private outdoor terraces in the entire Bellaire Tower. Owning the full floor provides uninterrupted … Continue reading A Great Deal in Russian Hill: Unit Sold for $545,000 Under Asking

San Francisco Real Estate Update June 2026: Record Prices, Shrinking Inventory, Fast Sales

Quick Take: Single-family homes breach the $2.2 million mark for the first time San Francisco’s single-family home market continues to reach new heights, with the median sale price climbing 22.56% year-over-year to $2,200,000. This marks one of the strongest year-over-year gains we’ve seen in the market’s recent history. The condo market posted more modest gains, … Continue reading San Francisco Real Estate Update June 2026: Record Prices, Shrinking Inventory, Fast Sales

A Great Deal in South Beach: Unit Sold for $105,000 Under Asking

A recent transaction on Folsom Street shows that opportunities still exist for buyers paying attention. The property at 488 Folsom Street originally asked $5,500,000. The final sale price came in at $5,395,000. That is a noticeable underbid for a premium high rise unit. The primary attraction of this property is the corner floorplan with ten … Continue reading A Great Deal in South Beach: Unit Sold for $105,000 Under Asking

A Great Deal in Miraloma Park: Home Sold for $198,000 Under Asking

Finding a true deal in San Francisco real estate feels like searching for a needle in a haystack. Most buyers want a perfectly staged home that is ready for move in on day one. When a property comes with a complicated situation, the buyer pool shrinks rapidly… leaving a massive opportunity for anyone willing to … Continue reading A Great Deal in Miraloma Park: Home Sold for $198,000 Under Asking

Massive Discount in Alamo Square: Home Sold for $1,875,000 Under Asking

Look at this incredible price reduction. The seller originally wanted $11,000,000 for this striking property. It ended up closing for $9,125,000 after sitting on the market for over a hundred days. We have to ask if this was the deal of the century or just a necessary market correction… You might think a huge price … Continue reading Massive Discount in Alamo Square: Home Sold for $1,875,000 Under Asking

A Great Deal in Russian Hill: Home Sold for $1,182,875 Under Asking

Sometimes the market hands you an absolute gift… you just have to be ready to act. We absolutely love seeing a buyer walk away with over a million dollars in savings on a premier piece of real estate. That is exactly what happened at the residence on 1100 Union Street #1000. The initial asking price … Continue reading A Great Deal in Russian Hill: Home Sold for $1,182,875 Under Asking

A Great Deal in Russian Hill: Home Sold for $2,600,000 Under Asking

A recent transaction on Montclair Terrace caught our attention. The listing originally asked $12,500,000 before eventually closing at $9,900,000. That represents a significant price reduction. People tracking sales might appreciate the closing number here… a major shift from initial expectations. The property carries a recognized architectural background, having been designed in 1938 by Gardner Dailey. … Continue reading A Great Deal in Russian Hill: Home Sold for $2,600,000 Under Asking

San Francisco Real Estate Update May 2026: Double Digit Gains and Lightning Fast Sales

May is fully upon us, and while the city might be getting a bit windier, our local real estate market is absolutely on fire. Even as we push deeper into the prime spring selling season, the housing scene is showing no signs of cooling down. Median sale prices are climbing at an extraordinary rate. Single … Continue reading San Francisco Real Estate Update May 2026: Double Digit Gains and Lightning Fast Sales

A Great Deal in South of Market: Unit Sold for $220,000 Under Asking

The property at 765 Market Street #25G recently sold for $2,275,000. Originally asking $2,800,000 back in 2024, the asking price eventually fell to $2,495,000 earlier this year. The buyers saw an opening… and negotiated an impressive $220,000 reduction from that final list price. This extensively remodeled residence features full slab Calacatta marble surfaces throughout the … Continue reading A Great Deal in South of Market: Unit Sold for $220,000 Under Asking

A Great Deal in Yerba Buena: Unit Sold for $150,000 Under Asking

They listed it at $2,300,000. It sold for $2,150,000. That’s a $150,000 discount on a high-rise condo at 301 Mission St in San Francisco… and someone walked away with it. The unit closed coming in at 93.48% of the asking price. At $990.78 per square foot for a generous 2,170 square feet, this was already … Continue reading A Great Deal in Yerba Buena: Unit Sold for $150,000 Under Asking

A Great Deal in South Beach: Home Sold for $10,000 Under Asking

The property at 461 2nd Street #355T recently closed below the asking price. Originally listed at $675,000, the final sale concluded at $665,000. Securing a space in the ClockTower Building with authentic brick and timber details for under the initial figure is quite the outcome. Finding a loft with soaring ceilings and original architectural elements … Continue reading A Great Deal in South Beach: Home Sold for $10,000 Under Asking

A Great Deal in South of Market: Home Sold for $198,000 Under Asking

The property at 1066 Bryant Street initially listed for $2,998,000. It recently closed at $2,800,000. Buyers secured a substantial $198,000 discount on this live work building. The most striking detail is the greenhouse style pent room. That upper level opens directly onto an expansive roof deck providing massive open air space. Getting that kind of … Continue reading A Great Deal in South of Market: Home Sold for $198,000 Under Asking