Time travel back to sub 3% interest rates with an Assumable Mortgage

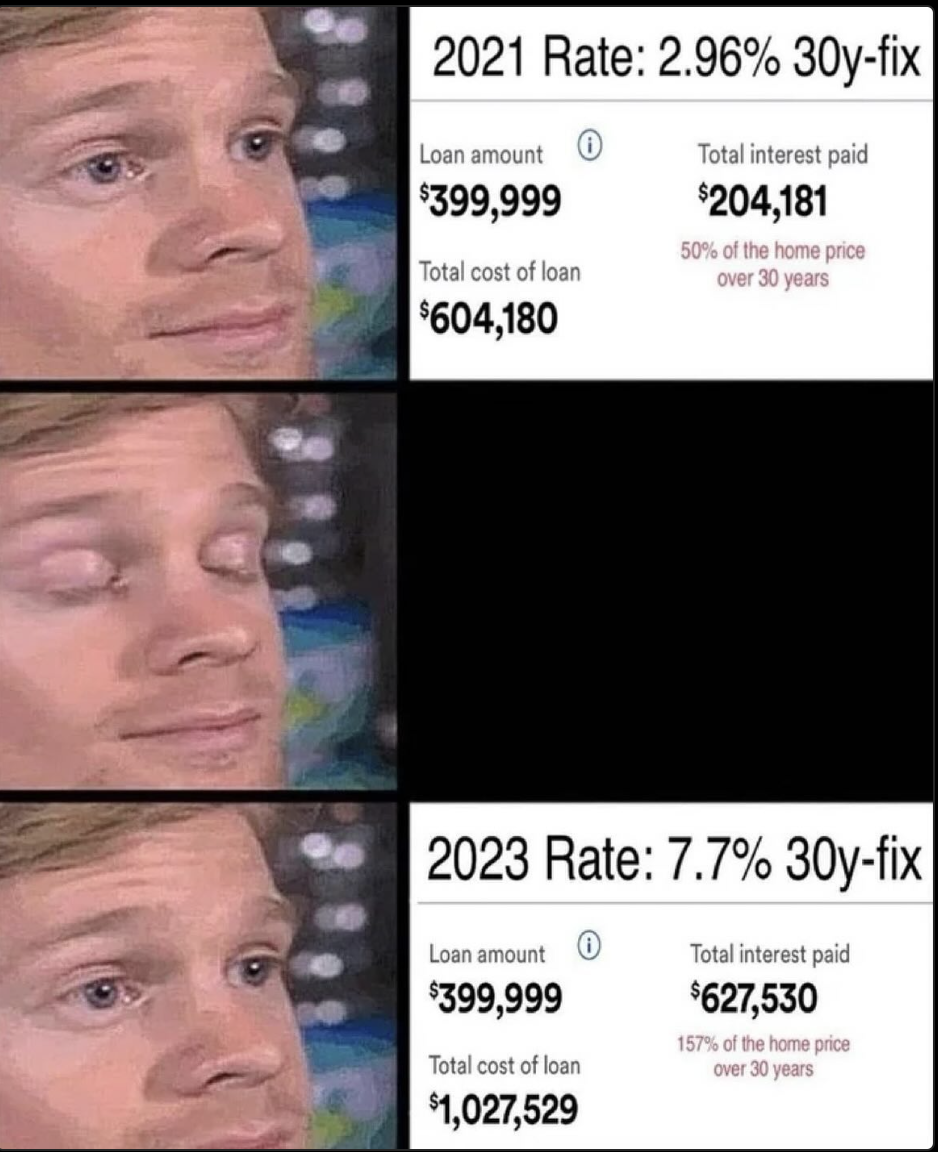

The real estate market has been extremely volatile and downright prohibitive to buyers (especially first time) in our local market over the past few years. Ever present single digit inventory has kept prices high and formerly uncomfortable, now borderline exorbitant interest rates have all but halted new loans. The majority of homeowners sit in the same conundrum of buyers, if they plan to buy back in on a new home they’ll likely paying twice as much interest as their current mortgage, with 82% feeling “locked in” by their low rate.

What if there was a way to purchase a home along with their attached low rate and term, wouldn’t that solve at least part of the problem? Similar to taking over a lease on a new car, there is a way with an Assumable Mortgage. 14+ million people refinanced during “The Great Pandemic Mortgage Refinance Boom” locking in at historically low rates. Depending on the type of mortgage, a current buyer may just be able to takeover payments if they meet the lender’s criteria and have the cash to cover the difference on any equity that has been accrued.

To put things in perspective, a 1 bedroom, 650’ sq foot Potrero loft bought in 2019 and this 2600’ sq foot house in Hercules with an assumable 2.65% mortgage have almost identical mortgage payments.

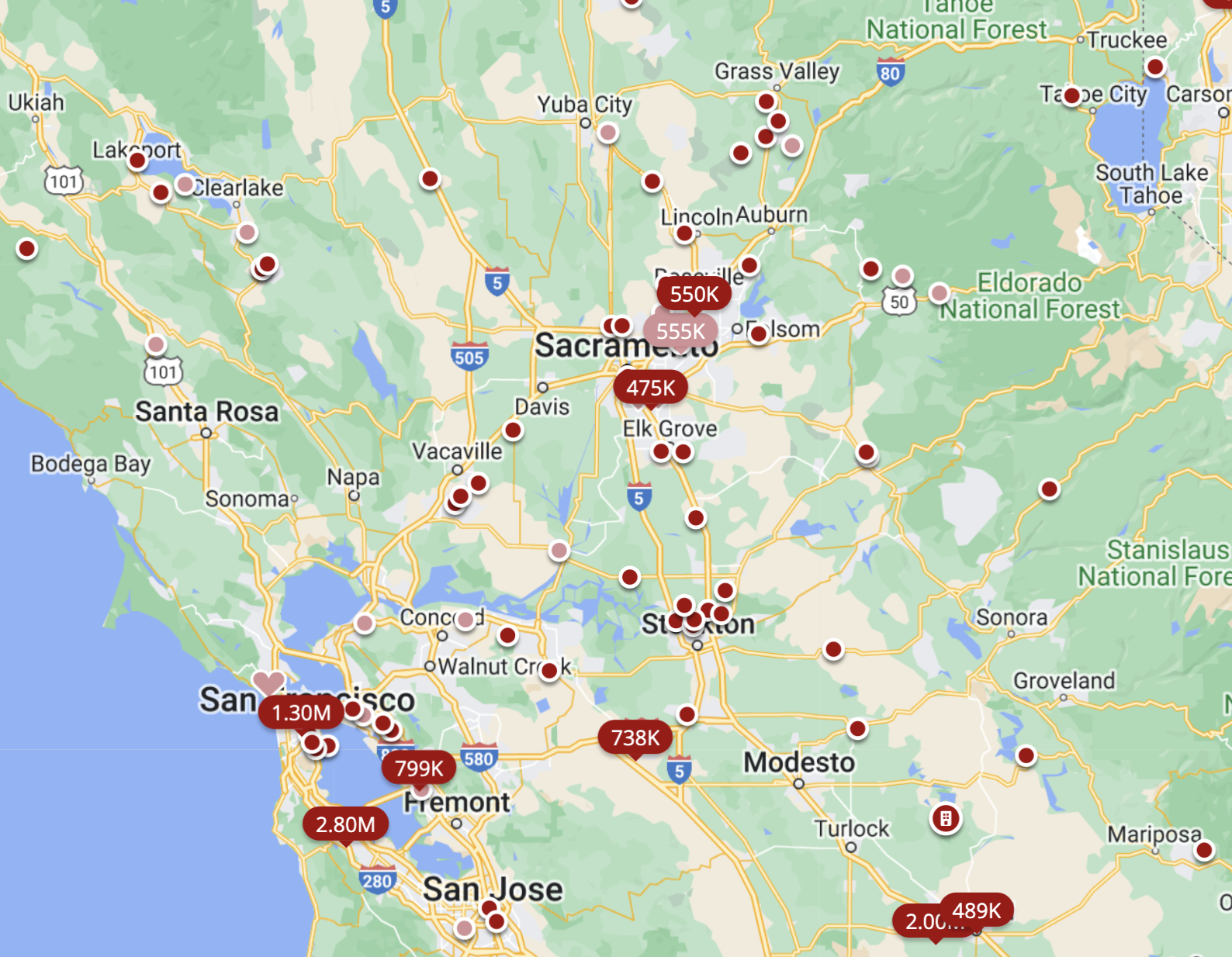

To start, only VA, FHA and USDA loans are assumable. Conventional and jumbo loans, the majority of current loans in our market, aren’t assumable. Adjustable Rate Mortgages are also assumable but since they are not locked in they probably aren’t worth the effort of pursuing. The Hercules home happens to have a VA loan. That being said, there are plenty of homes with assumable mortgages in desirable area’s like the Foothills and surrounding areas, as seen below:

Now what does it take to actually assume a mortgage and why isn’t everyone doing it?

1. Cash. You’ll need a fair amount of cash on hand to pay the owner in order to cover the amount they have paid off on their loan. If a home is $950k and their loan is $750k you will need $200k in cash to even start the conversation. Most purchase contracts in the Bay Area come with a 20% down payment, so coming up with that difference isn’t overly intimidating to buyers in our market. Now if that home has accrued $400k of equity then the potential assumer’s will need a substantial amount more of cash to acquire that dream loan, but since most loans were refinanced in the past couple years there is a strong chance that a home doesn’t need much more than 20%.

2. Meet lender requirements. The new potential mortgagor will need to qualify for that loan much in the same way they would for any home loan, albeit the debt-to-income ratio will be much more lenient since they would be saving close to double per month by getting a 21’ rate.

3. Must be owner occupied. An investor can’t assume a mortgage and it must be the homeowners primary residence.

4. Lenders aren’t screaming from the roof tops with a list of assumable mortgages on offer, they don’t have much to gain from these bygone rates, but not too fear, there are few startups working on a way to make it easier for prospective homebuyers and sellers to leverage this unicorn scenario. Both assumable.io and withroam.com are platforms built around making this connection a reality. Last but never least, a savvy realtor always knows where to look ;)

So how does this effect prospective Bay Area buyers? I personally have plenty of clients who are dying to get into the real estate but renting it out on the sidelines waiting for rates to hopefully dip. I also know that a 10 acre property with an assumable $2600/ month mortgage piques their interest much in the same way a turn key Grass Valley forever home does with a sub 8% assumable rate, it gives them an opportunity towards home ownership at a palatable price point.

If you’re interested in homes that have assumable mortgages or have questions about this type of scenario please do not hesitate to reach out. I pride myself on being an unconventional thinker and am always happy to share what I’m seeing in our ever changing market.

Bryce Adams

theFrontSteps Real Estate

DRE# 02133765

@bryceadamshome

415-497-6153

[email protected]

“Buying or selling a home can bring on both exhilaration and sleepless nights. With a strong understanding of the local market, Bryce is in the best position to help you navigate what can seem like an overwhelming number of options and considerations.“