by Bryce Adams

If I knew where things were headed, I most likely wouldn’t be sitting on my computer blogging about what the market is or isn’t going to do, or maybe I would be, relishing the moment. That being said—everyone loves to speculate, but, there is significant data and factors that have framed my outlook. It might be obvious to some or contradictory to others, but my only goal is create a dialogue and potentially see a holistic perspective.

Unsurprisingly, my SOI (sphere of influence) tends to be my peers: late twenties to early fifties. I fall in the (sweet?) spot—quickly approaching the big four-zero, 40. I’m either asked or told daily how the market is doing, where it is going, and if it is going down or up. Now most of my friends, acquaintances, peers, etc., are either in the early stages of their family and already have a home or are beginning down the path of family/marriage and are looking to purchase their first home.

It is important to note that “our” parents (cough, Boomers) most likely purchased their first and often only home with a mortgage close to triple what the current interest rate is. From 1974 to 1992 the rate (nationally) was never better than 8.39% and as high as 16.63% (1981). To put that in perspective, $300k in 1981 was equivalent to $970k today. Also worth noting, a $300k home in 1981 is probably worth well above $970k, probably 2.5x+ if its in SF/Marin.

Now these two groups of “already own” and “first time buyers” sit on very different edges of the current buyer fence. The first most likely bought pre-pandemic and are benefiting from massive appreciation in their home value (to the tune of 40%), while the other is left jaw agape at what “coulda/shoulda” happened if any number of factors had been at play. It’s a double edged sword for the first group, as they have now potentially doubled their investment but are playing in the same pool as the second group, albeit with twice the equity. What that means is that if they want to leverage their equity and level up into a bigger/nicer home in the same area, then they are buying in at the same premium the second group is, higher property taxes (1% of purchase price) and all. A few friends have moved out of state: renting their Bay Area home, easily covering their mortgage, and putting their $800k+ Bay Area “starter” home towards purchasing a turn-key “forever” home—albeit in a less desirable area, just based off home prices. ;)

So, where does that leave the Marin and SF single-family home market? There are dozens of contributing factors to where the economy sits today: massive inflation, looming recession, Russia/Ukraine war, COVID-19, rising interest rates, volatile stock market, supply chain headaches, hiring freezes, another election—the list goes on. Some factors are directly influenced by each other, whereas a few have been unpredictable curve balls. The Russian war & COVID-19 weren’t necessarily predicted, but their effects on the following were: the stock market wasn’t going to maintain its pace, interest rates were never going to stay low forever, and supply chain issues are directly related to mandatory quarantines.

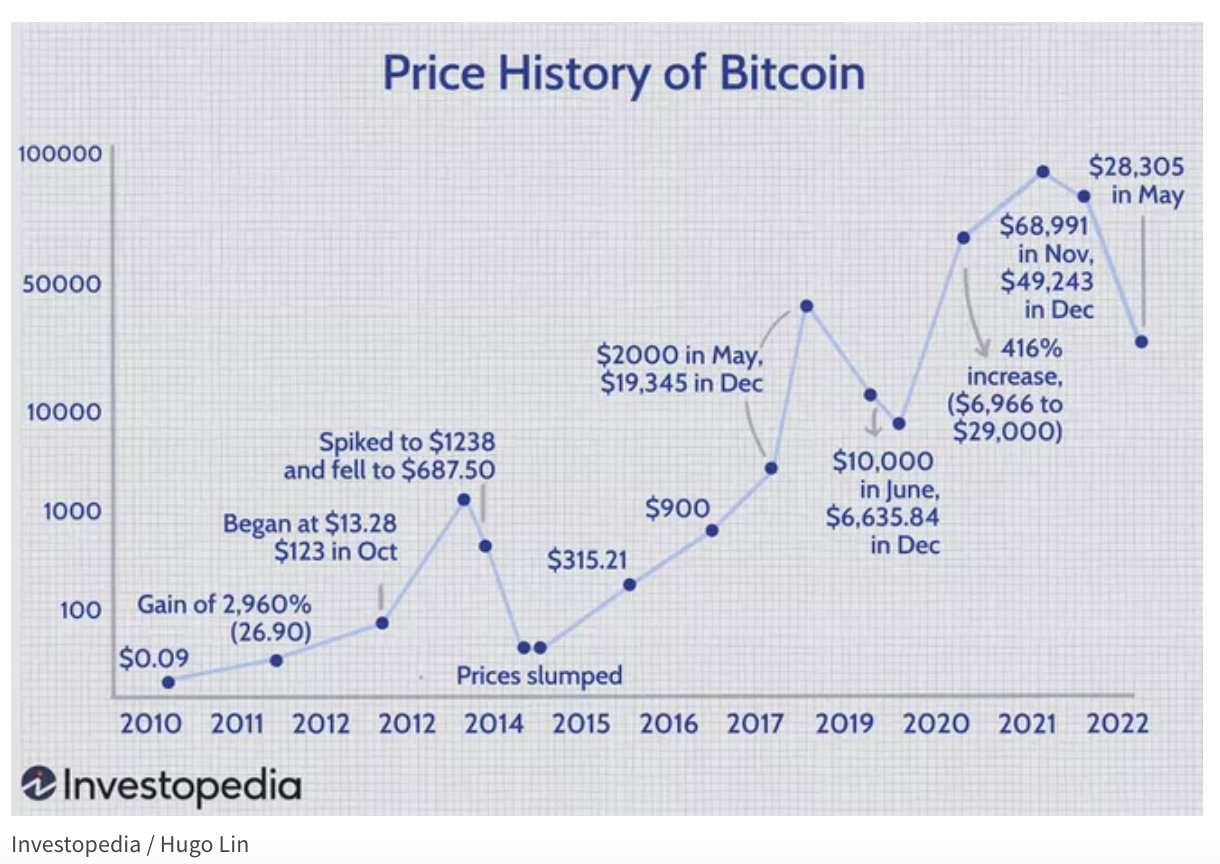

Most relevant to single-family homes in Marin and SF are interest rates, stock market, and hiring freezes. Understandably, everyone loves to gripe about the current rise in interest rates. They are “high” right now, much in the same way Crypto is “down” right now, but from my experience and interactions people tend to be very near-sighted when comparing these things. Crypto is greatly down compared to a year ago, but retrospectively it is up. Much in the same way interest rates are not all that dire compared to the last 50 years.

I empathize with anyone who panic bought either crypto or real estate in the past 2-years as that has probably been a wild ride and uncomfortable financial position to be in today. The COVID-19 wave that these two industries rode was completely unsustainable and we are now seeing a leveling off or cooling of what was essentially a faux ride. What I personally don’t foresee is a significant decrease in single-family home-value for a few reasons.

- Inventory will always be an issue in San Francisco and Marin.

- Lenders are not writing bad loans, they’re being more conservative on who they finance.

- Yes, homes that were sold during the pandemic for 50% over-asking might not be appraised at what they sold for today, but there is usually a disconnect between asking and selling price in those scenarios. I wager there is a very small percentage of homes that are appraised for less than what they listed at (as compared to what they sold for). This is a complete 180 from what the market is currently doing now: homes are selling for asking-price and if they are sitting longer than 2-weeks you can see significant price reductions—leading to a quick-sale.

- The economic engine that drives these values is still strong in the Bay Area, and companies are realizing that WFH is a “need to have” not a” nice to have.” People that might need to be in the office a few times a week or month now have the ability to move to a more desirable location versus something that is daily-commute friendly.

- The stock market is bearing down and batting its hatches, but this isn’t necessarily as impactful on the single-family home-market as it is for the luxury ($3M+)/vacation home-market. Yes, your IRA isn’t going bananas like it was last year, but that doesn’t mean these companies are paying any less. Sure, they might not be hiring at-will or throwing extravagant holiday parties, but if you’re working in the Bay Area, you most likely will have one of the better salaries in the nation.

- Millennials are the largest generation and therefore the biggest purchasers of real estate, for every family bailing to South Carolina there are a dozen vying to live the Bay Area dream.

So where does that leave us? Do I think the market is cooling? Yes. Do I think home prices are falling? That’s a loaded question, but overall no. I think they are correcting, not falling. I don’t foresee a scenario where a 1500′ sq foot home (@$1k/sq ft) suddenly becomes worth $1M or less. If you bought a 1500′ sq ft home for $2M then, yes, you might feel some pain for a year or more while things settle. Overall, low inventory is such a significant factor that I do not see a massive decline in home values for San Francisco and Marin.

So how does this help me buy a home?

- What you see is what you get. Listing and selling prices are finally more aligned.

- Contingencies exist for a reason and are back on the negotiation table, don’t be afraid to use them.

- Lenders want to help you get a loan—the hack is that you can always refinance.

- If you are in a position to entertain the idea of buying, and have enough saved for a deposit, then it is usually a safe time to buy.

Attempting to time the market is a slippery slope and there will always be unforeseen curveballs, but inventory in Marin and San Francisco will always be a significant factor contributing to home value.

Working with a local agent is the best way to make sure you are searching and spending efficiently. I welcome the opportunity to learn more about your real estate aspirations.

As always, if you have any questions you can contact us directly, or throw them in the comments below. Make sure to subscribe to this blog, or follow us on social media @theFrontSteps (Instagram, Facebook). And please do consider giving us a chance to earn your business and trust when it’s time to buy or sell Bay Area property. People like working with us, and we think you will too.

Bryce Adams

theFrontSteps Real Estate

DRE# 02133765

@bryceadamshome

415-497-6153

[email protected]

“Buying or selling a home can bring on both exhilaration and sleepless nights. With a strong understanding of the local market, Bryce is in the best position to help you navigate what can seem like an overwhelming number of options and considerations.“

Thanks for writing this Bryce. I have not seen much writing about the topic recently, to my surprise. I appreciate your writing

Great article Bryce. Keep them coming.

Well written and informative. There will always be a barrier to entry; whether it is home prices, down payments, or rising interest rates, but the next two quarters look like a good time to take advantage of relatively low rates, lower 1-2yr prices, and new lending options. Thanks for the info Bryce!