Like Warren Miller always says, “Now it’s time for one of these…Intermission”. In my case, an intermission from blogging. Back to normal programming in early 2016. This site will also be undergoing a redesign, so if you happen to land here when it looks totally weird, and possibly not working properly, please be patient, and … Continue reading Time For An Intermission

Tag: Selling A Home In San Francisco

New Case-Shiller reflects continuing appreciation of SF Bay Area home prices this spring

The new April Case-Shiller Home Price Index for the Bay Area counties of SF, Marin, San Mateo, Alameda and Contra Costa, released 7/7/15, reflects the middle of our spring market. (The Index is released 2 months after the month indicated.) All home price tiers saw further increases. Since the April Index is a 3-month rolling … Continue reading New Case-Shiller reflects continuing appreciation of SF Bay Area home prices this spring

SF Real Estate Market – Animated Charts

Against my will, I’m back from vacation, and back at it. So it’s on with the real estate show. This first chart below is a very simplified, approximate and smoothed out chart graphing the percentage ups and downs in San Francisco home prices over the past 30+ years. We have other charts that illustrate more … Continue reading SF Real Estate Market – Animated Charts

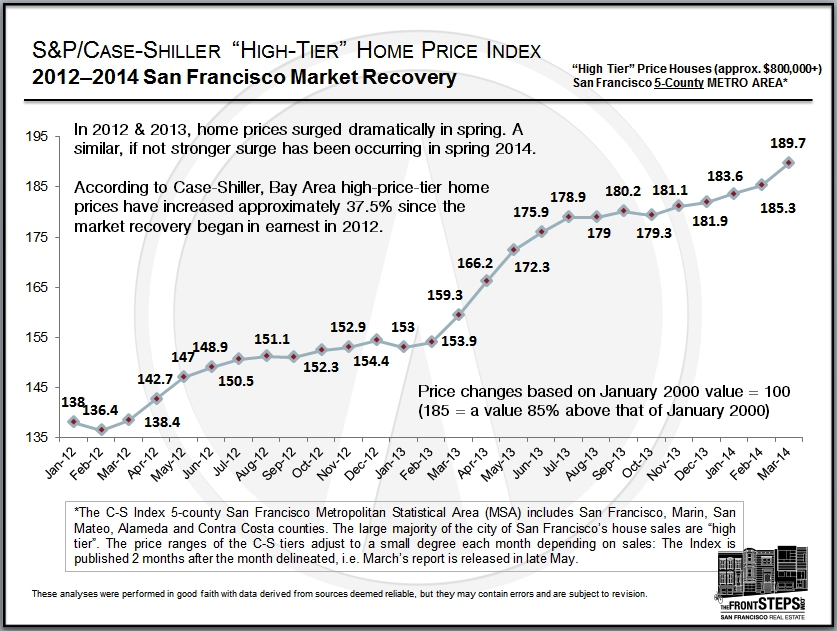

New Case-Shiller Shows Another Jump In Bay Area Home Prices – Up 37.5% Since 2012

The new Case-Shiller Index report for the 5-county San Francisco metro area, for March, is showing the same acceleration in home prices that buyers and sellers are experiencing in the market. The 2.4% increase from February to March 2014 is the largest since spring 2013, and further significant increases are expected in the Index reports … Continue reading New Case-Shiller Shows Another Jump In Bay Area Home Prices – Up 37.5% Since 2012

Home Ownership as an Investment, Home Prices, Inflation, Leverage & Home Equity

First and foremost, any home purchased needs to work as a home: it fulfills your housing needs at an affordable monthly cost – ideally, a cost, after tax deductions and principal pay-down, less than or similar to that of renting the property. However, though it cannot be compared on an apples-to-apples basis to investments such … Continue reading Home Ownership as an Investment, Home Prices, Inflation, Leverage & Home Equity