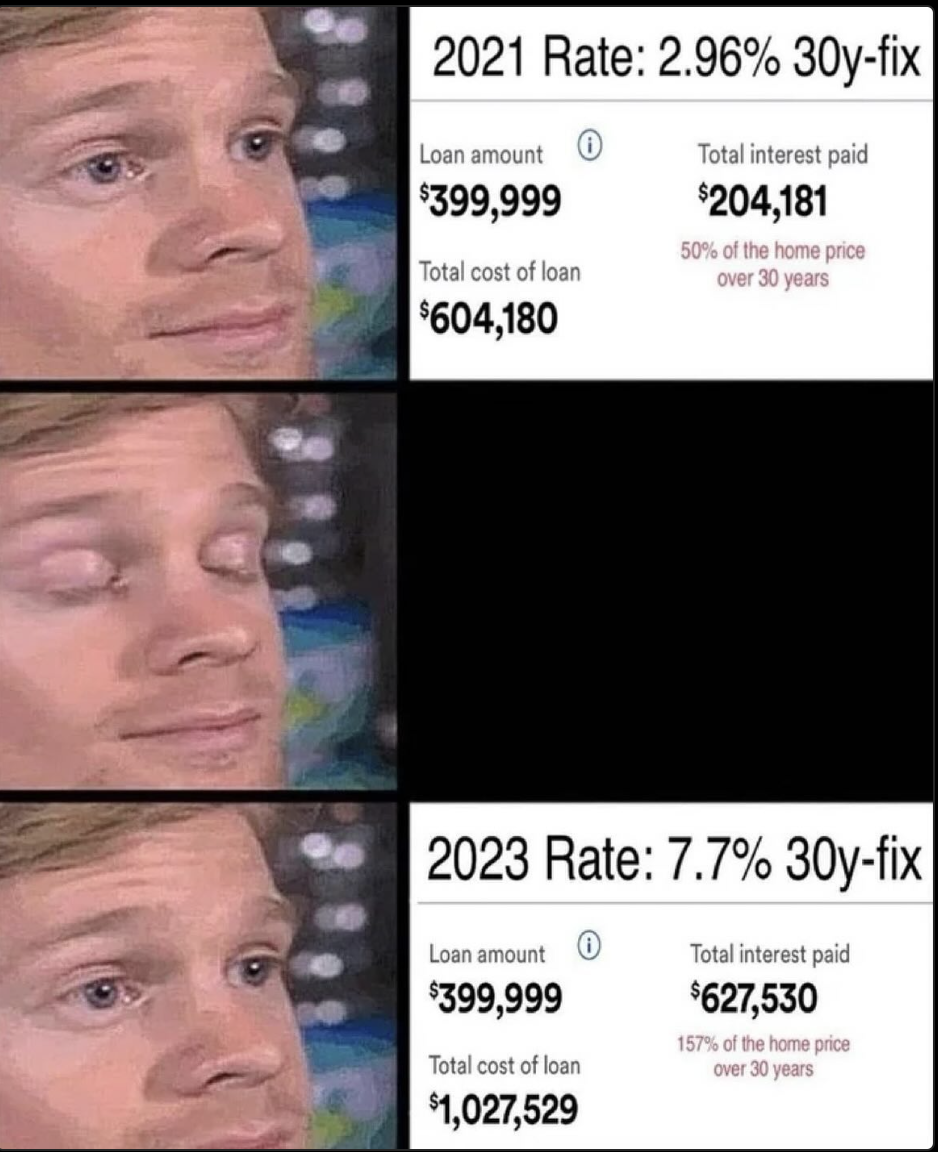

It’s that time of year…numbers from the prior year come in, get crunched, and speculation for the coming year begins. There is a TON of data and resources to search, and you can read and try to time real estate all you want. We’re just here to narrow it down for you and guide you along the … Continue reading A 1.18% Mortgage Rate Drop Matters … A LOT!

Category: Mortgage/Rates

How to Hack the Current 7%+ Interest Rate

How to Hack the Current 7%+ Interest Rate

Time travel back to sub 3% interest rates with an Assumable Mortgage

“It’s always better to buy real estate and wait than to wait and buy real estate.”

Being a real estate agent is akin to being a fitness, finance, political anything, etc guru thanks to social media. You can, without much resistance, say whatever, however, you want in order to portray yourself or your agenda in a certain light, shout out to Top Producers in their bio and nod to Mr. Musk … Continue reading “It’s always better to buy real estate and wait than to wait and buy real estate.”

Does The Fed Rate Cut Mean Lower Mortgage Rates For Your Home Loan?

Surely you heard the news yesterday the “Fed is going to cut interest rates” again, and you might think that means lower interest rates on your home loans. Well…it isn’t so cut and dry. For an explanation, we asked our go-to mortgage broker, Tim Wood of Opes Advisors for a little clarification: What the Fed … Continue reading Does The Fed Rate Cut Mean Lower Mortgage Rates For Your Home Loan?

Will Interest Rates Rise?

One of my preferred mortgage brokers (Tim Wood @ Terra Mortgage) just sent me his newsletter that dives into the question of whether interest rates will rise in 2017. It’s so full of interest rate chatter about Feds, Reserves, Trump, yada, yada…I figured you’d all love it. So here you go: Are You Sure that … Continue reading Will Interest Rates Rise?

Home Ownership as an Investment, Home Prices, Inflation, Leverage & Home Equity

First and foremost, any home purchased needs to work as a home: it fulfills your housing needs at an affordable monthly cost – ideally, a cost, after tax deductions and principal pay-down, less than or similar to that of renting the property. However, though it cannot be compared on an apples-to-apples basis to investments such … Continue reading Home Ownership as an Investment, Home Prices, Inflation, Leverage & Home Equity

So How Low Are Interest Rates?

Interesting tidbit about interest rates should you be considering purchasing a home. Could they get any lower? For more details you can click here. You’ll be taken to a newsletter from my go-to mortgage broker, Tm Wood. He’s good, the market is good, rates are good, the snow is (getting) good, it’s all good.

San Francisco Housing Market Not Stopping…How’s That For A Gift From Santa!?

In this season of giving and being thankful, I’d have to say that San Francisco Bay Area residents should be pretty thankful that our market is nowhere near that of the national average. If you’re a seller you can be thanking your lucky stars that buyers are out there in droves, and if you’re a … Continue reading San Francisco Housing Market Not Stopping…How’s That For A Gift From Santa!?

Reader Reports: We Finally Were Able To Refinance! What A Nightmare! And Some Advice…

From a reader: Dear theFrontSteps, After TWO YEARS of intensive search and questioning and hunting ….we closed yesterday on our refinancing! We got a $600,000 loan at 4.5%. (no point, no refinancing costs, except for appraisal and recording fees). By the way, the appraisal came back at $1,200,000, which made us laugh a good time. … Continue reading Reader Reports: We Finally Were Able To Refinance! What A Nightmare! And Some Advice…

Here We Go Again With The Lending

Intercepted from inter-office emails: Great News, We are now offering Fannie’s new HomePath loan program! Let your clients know these improved loan terms to generate new business. Essentially, the program has the clients using Fannie loans to buy foreclosed properties owned by Fannie, therefore Fannie gives improved loan terms to the buyer. PROGRAM HIGHLIGHTS: -97% … Continue reading Here We Go Again With The Lending

Loan Limits Raised To $729,750, It’s Official *

*-at some banks

FHA Checklist For Spot Loan Approvals

We get a lot of questions about FHA loans these days, particularly if we know what buildings will qualify for FHA loans in San Francisco. There is a simple answer to that question, “No, we don’t know.” But other people do, and those people are loan experts…mortgage bankers/brokers… and luckily they feed us information to … Continue reading FHA Checklist For Spot Loan Approvals

Ask Us: Refinancing And Appraisals, When The Banks Aren’t Helpful Turn To The Blogs!

Where readers ask, and we (the community) try to answer: I appreciate all the general information I get from this terrific blog. This is my first question about my own situation. I’ve been negotiating with the major bank (WellsFargo) that holds my first ($498K) and second ($14K) for a refinance from a 5.5% ARM to … Continue reading Ask Us: Refinancing And Appraisals, When The Banks Aren’t Helpful Turn To The Blogs!

So How Much Does A Buyer REALLY Need To Put Down

As our regular readers know, we get every type of question under the sun, most of which we post directly to the site and let the community answer. Sometimes answers aren’t so cut and dry and there are certainly differing opinions. One very common question these days is “How much money do I need to … Continue reading So How Much Does A Buyer REALLY Need To Put Down

Ask Us: Remaining TIC Fractional Lenders

Where the readers ask and we (the community) try to answer: Hi, just come across your site, very informative. I’m trying to find TIC Fractional Lenders for a 3 unit + 1 unwarranted [unit] building in SF. We purchased it last October, have completed our renovations, 2 units will be owner occupied. We’re planning to … Continue reading Ask Us: Remaining TIC Fractional Lenders

Reader Reports: Who’s Getting Your Loan Approved And Why?

“San Francisco’s number one closer”: While you’re at it: http://abclocal.go.com/kgo/video Once you are at the link, look for the “7 On Your Side” tab in the Video Library part of the webpage and click it. You’ll see a picture with the heading “Marketing Ploy Disguised as Government Offer” and a HUGE Mike or Darius. That’s … Continue reading Reader Reports: Who’s Getting Your Loan Approved And Why?